Here's how we can help

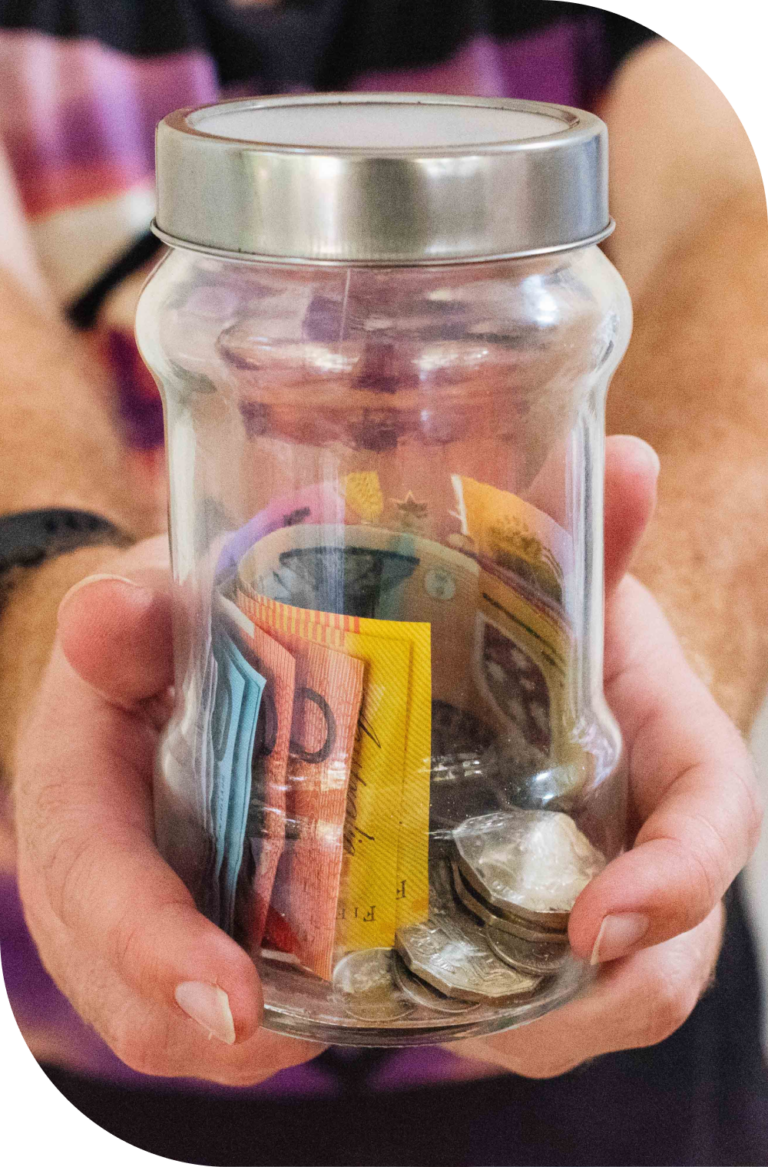

Saving for your deposit

Buying a house is exciting and life changing. What’s not fun is saving for a deposit.

In recent years, surging house prices have made the size of a deposit required just that much harder to get together. With some discipline you will have a deposit for your home in no time. There are two ways to save your deposit faster; save more or spend less. It’s that simple.

Here are some ideas to get you started on the path to home ownership

Work out your budget

Household living costs are also on the rise so it’s time to stop and look at how you spend your money and what big ticket items with small value you can do without or reduce. The key is to budget sensibly by putting together a realistic savings plan that doesn’t compromise your family’s lifestyle too much.

Prepare a budget and stick to it. It’s a great way to understand your full financial position and how much you will need to save towards your deposit. Estimate your regular expenses; such as transport, groceries, lunches, childcare. Don’t forget any debts, including credit cards, car loan or anything else that you have to make repayments on. The hardest part is identifying and cutting out unnecessary expenses. Work out what luxuries you enjoy that you can reasonably afford to give up.

Manage your debts

Over time, it’s easy to build up small debt here and there. Individually they may not seem like a lot but you may be paying higher interest rates already and a lot of extra fees which could keep you in debt longer and impact your lifestyle.

There is no doubting the convenience of credit cards when you are running a little short. They’re handy to use and accepted almost everywhere. But do you really need one? If so, how many are you using? And what about personal loans, car loans and interest-free purchases? Remember, you can’t save effectively if you are paying off debts. So cut down on those credit cards, consolidate your debts and do everything you can to become debt free.

Sort out your banking

Most banks charge fees on their accounts. For a first home buyer just starting out, the most popular form of saving is to open up an at-call deposit account. These lenders include the traditional lenders, such as banks, building societies and credit unions.

It’s great to choose an account that pays good interest, but there are other factors you should consider, such as account-keeping fees, transaction costs, when interest is calculated and accessibility.

Make an appointment with us today and get started on the road to your first home!

Your Think & Grow finance advisor will...

Understand your needs and Goals.

Compare hundreds of bank products from over 40 lenders and determine the loan that best suits your needs.

Calculate your maximum borrowing capacity and work out your maximum purchase price based on the funds you have saved.

Outline all fees and charges associated with buying your home.

Research the level of first home buyer Government grant you may qualify for.

Advise your minimum repayments and discuss principal and interest versus interest only repayments.